Critics of the Dodd-Frank Act argue that the new regulatory regime has weakened small banks (see, for example, Peirce, Robinson, and Stratmann). This criticism is echoed in the Financial CHOICE Act—proposed by House Financial Services Chair Jeb Hensarling—that would largely scrap the current oversight of large systemic intermediaries in part to reduce the regulatory burden on “community financial institutions” (those with fewer than $10 billion in assets).

We share the goal of ensuring that regulation is cost effective for small banks that pose no threat to the financial system. However, we do not believe that the Dodd-Frank oversight regime of the largest, interconnected, complex intermediaries is a principal driver of the challenges facing most small banks.

Instead, we note that the decline of small banks has been going on for more than 30 years, decades before the Dodd-Frank Act became law in 2010. This decline has been and remains concentrated in the very smallest institutions. Furthermore, in our view, the parts of Dodd-Frank that are seen as adding most to the costs facing small banks—while important and worthy of support—have little to do with systemic risk. A cost-benefit analysis of microprudential regulations that takes account of the special needs of the smallest banks could reasonably address these issues.

Our conclusion is clear: there is no reason to relax systemic oversight of large intermediaries for the purpose of easing regulatory burdens on small ones.

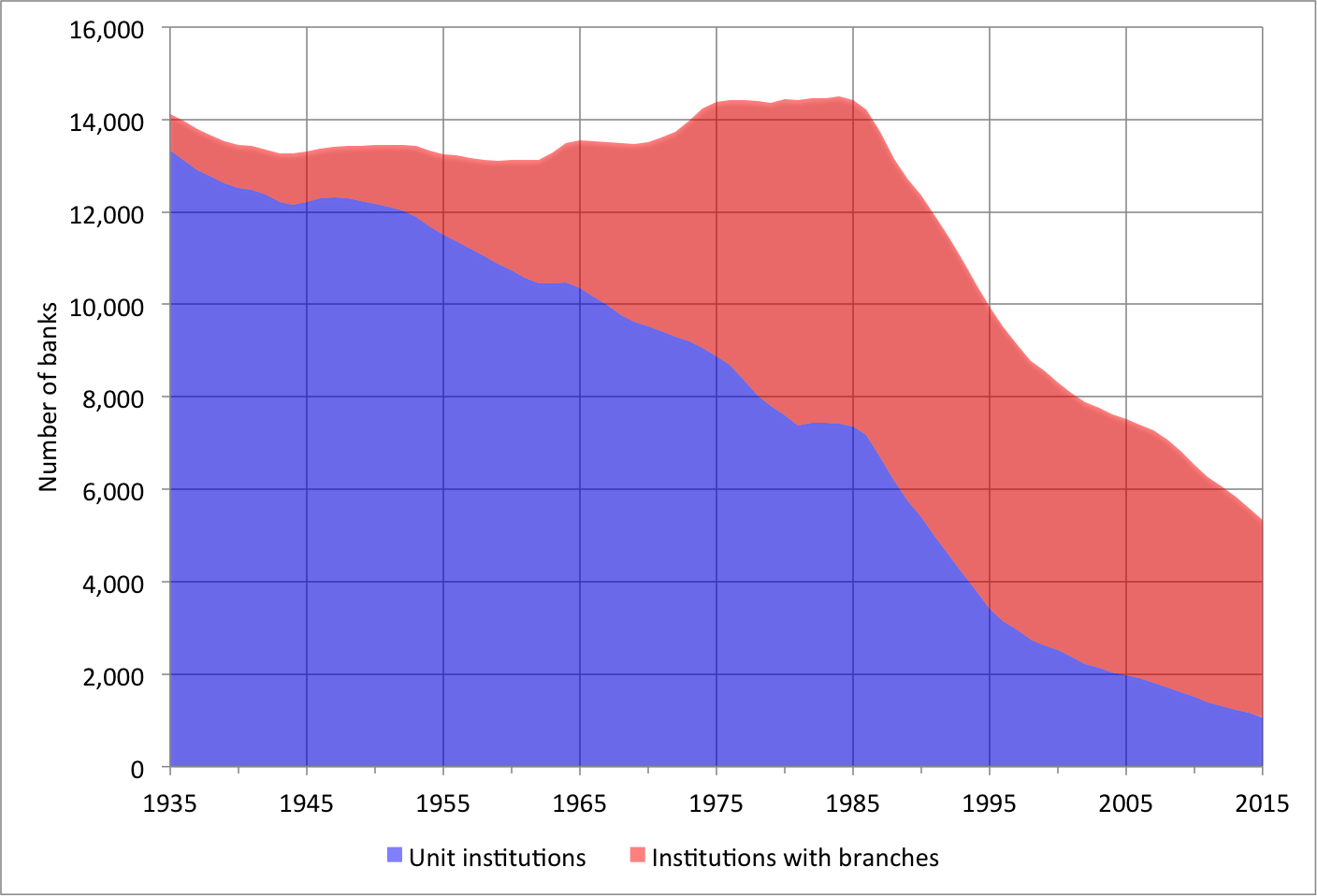

To understand the ongoing consolidation of the U.S. banking system, we start with a bit of history. State and federal laws preventing competition both within and across states helped sustain the presence of around 14,000 insured banks for more than 50 years after the Federal Deposit Insurance Corporation (FDIC) was created in 1934 (see chart below). Most of these were “unit banks” with only a single branch. State restrictions on interstate banking—underpinned by the McFadden Act of 1927 requiring national banks to abide by state laws—resulted in a highly fragmented, inefficient, and under-diversified banking system that imposed high costs on customers (see, for example, Jayaratne and Strahan).

United States: Number of FDIC-insured banks by type, 1935-2015

Source: FDIC Historical Statistics on Banking.

Beginning in the late 1970s, technological changes (such as competition from telephone banking) led states to begin easing entry barriers. This culminated in 1994, when Congress passed the Riegle-Neal Interstate Banking and Branching Efficiency Act that effectively ended state branching restrictions. Unsurprisingly, as the chart highlights, deregulation ushered in a period of sustained decline of the number of U.S. banks.

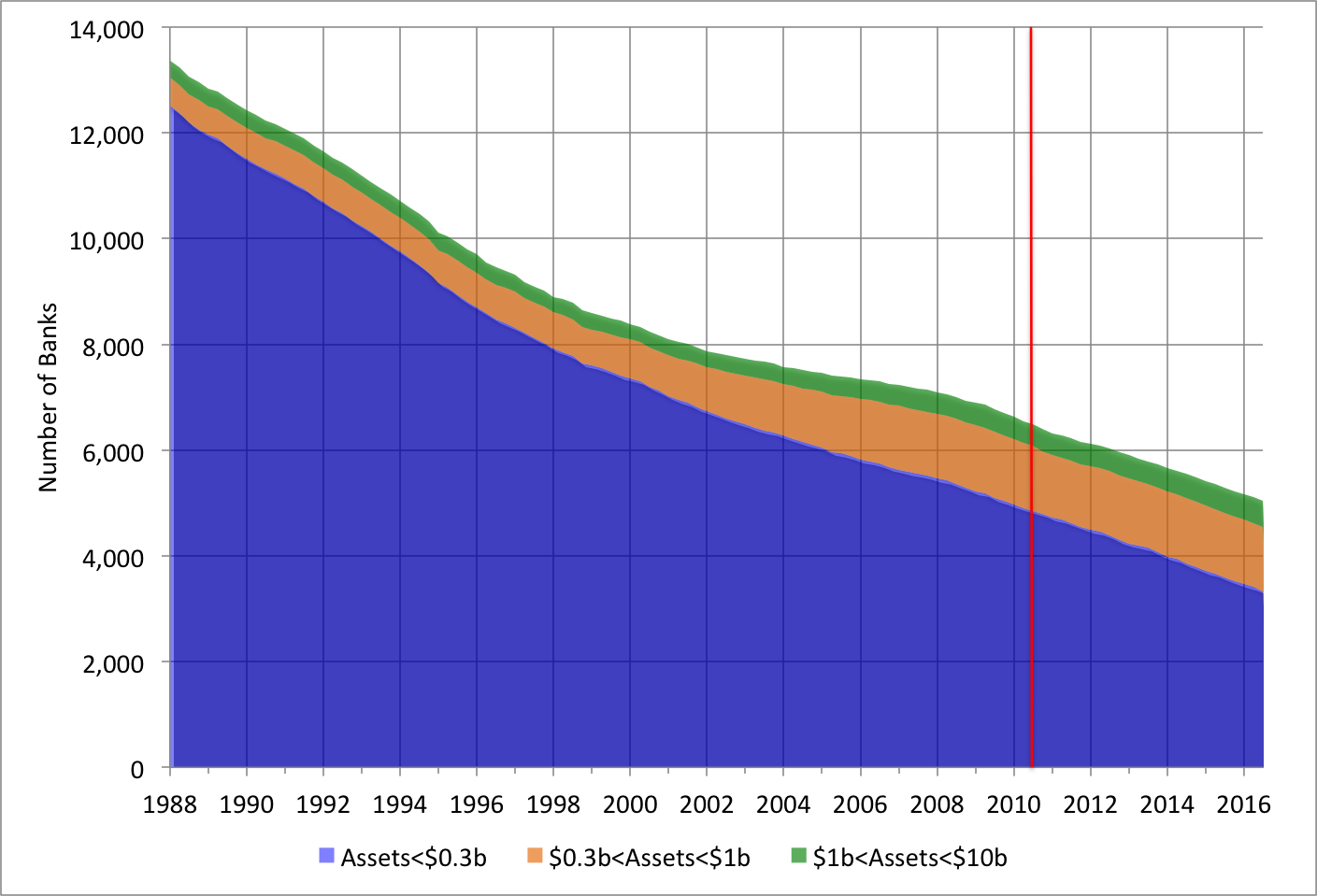

Importantly, virtually all of the consolidation in the past 25 years has occurred among the very smallest banks. Looking at the next chart, which only includes “community banks” with fewer than $10 billion in assets, we see that since 1988 the number of banks with less than $0.3 billion in assets has fallen from 12,509 to 3,335. Even so, these tiny banks still account for two-thirds of the community-bank universe. Importantly, the numbers of somewhat larger community banks rose sharply over this period: banks with assets more than $0.3 billion and less than $1 billion more than doubled in number to 1,227, while banks with more than $1 billion and less than $10 billion in assets increased by 55% to 497.

U.S. insured commercial banks by asset size, 1988-3Q 2016

Note: The vertical red bar marks the passage of the Dodd-Frank Act. Source: Federal Financial Institutions Examination Council, as available from FRED.

Importantly, the trajectory in the chart shows no shift with the 2010 enactment of Dodd-Frank. Since then, the very smallest banks continued to dwindle, while the two larger classes of community banks were either virtually unchanged in number or increased substantially.

This pattern suggests that technology advances such as online banking are far more important drivers of the numbers and mix of small banks than regulation. This is unsurprising since Dodd-Frank’s rules requiring stricter scrutiny of systemic banks apply only to institutions with greater than $50 billion of assets, not to community banks. Furthermore, banks with fewer than $10 billion in assets are exempt from the primary jurisdiction of the Consumer Financial Protection Bureau (CFPB), which was created by Dodd-Frank and is now a target of the CHOICE Act.

To be sure, the very smallest institutions are relatively more threatened by increased compliance costs. A 2014 survey of some 200 community banks found that since July 2010, the median number of compliance personnel doubled from one to two persons. Such fixed costs are a challenge for the smallest banks. According to Feldman, Heinecke, and Schmidt (2013), for banks with less than $50 million in assets, the median decline in the return on assets from increasing staff by 1 person is an estimated 23 basis points (compared to a median ROA of 61 basis points). For comparison, adding 3 persons to a bank with $500 million to $1 billion in assets lowers ROA by 4 basis points (compared to a median ROA of 87 basis points in this asset class).

The following table highlights this fixed-cost challenge. The smallest FDIC-insured banks—those with fewer than $100 million in assets—account for more than one fourth of insured banks but less than 1% of assets. And, while their funding costs (in basis points) are largely indistinguishable from most banks, a much larger share of them is unprofitable.

FDIC-insured institutions, 3Q 2016

Notes: Assets in billions of U.S. dollars; leverage is the ratio of the return on equity to the return on assets; funding cost in basis points. Source: FDIC, Quarterly Banking Profile, September 30, 2016.

Regardless of any changes in regulatory costs, the odds are that a number of these tiny banks already are too small to compete. A growing fraction also will face increased competition as their clients—principally in rural areas and small towns—shift to using more efficient technology such as mobile deposits and digital wallets that are provided at low cost by much larger institutions (see our related post).

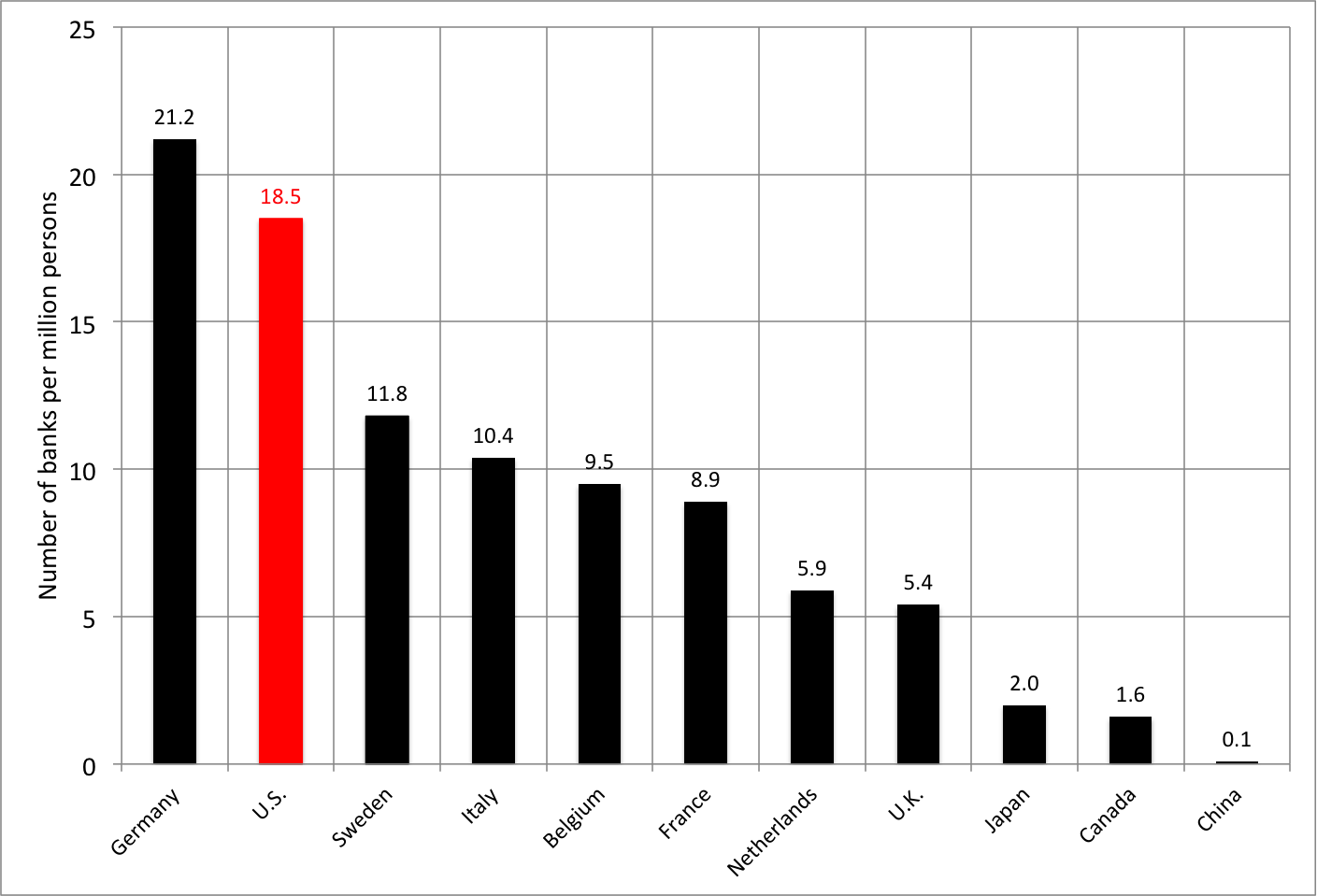

From an international perspective, further consolidation in the U.S. banking sector also would be unsurprising. The following chart compares the number of deposit-taking institutions per capita in the G-10 countries plus China (the U.S. observation includes only FDIC-insured institutions as in the table above). Along with Germany, the United States remains on the high side of this distribution. Even if all U.S. depositories with less than $300 million in assets were eliminated, the per capita number of U.S. banks per million persons would be 8.2, only slightly below that in France. (Eliminating all banks with less than $10 billion in assets would leave the number of banks at 2.3 per million persons, still more than Japan or Canada.)

Depositories per million persons (latest available data)

Note: The U.S. observation includes FDIC-insured institutions only. Sources: Bank of England, Bank of Japan, Canadian Banking Association, Chinese Bankers’ Survey 2015, ECB, FDIC, United Nations population data, and authors’ calculations.

Nevertheless, to ensure that regulation is not the cause of their demise, regulators should aim to reduce compliance costs for the smallest and simplest banks in the system. Tools for this purpose have existed for decades: for example, the Federal Reserve has always imposed lower reserve requirements on small banks. However, the biggest burden on these tiny institutions may be the increased reporting that all banks face: according to one analysis, since the 1970s, the number of items in the standard bank Call Report has risen from around 50 to nearly 2,400. That seems like overkill for a small-town, straight-vanilla bank whose greatest risks arise from simple loans to local firms (see Cole and White).

At the same time, while we support simplification for the smallest banks, it is important that the larger community banks remain subject to sufficient oversight to ensure that they do not become a burden on the public purse in the event of failure. Experience from the recent crisis shows that resolution costs for these institutions are far from trivial: of the 433 commercial banks that failed between 2007 and 2014, 430 were community banks with fewer than $10 billion in assets. The FDIC’s closure costs for these community banks totaled $43 billion (out of a total of $50 billion for all commercial banks).*

Finally, it is critically important to separate concerns about the systemic oversight of the largest, most complex and most interconnected bank and nonbank intermediaries from those about the regulatory burdens on the very smallest institutions. If these two goals are related, then it is because a credible regime that limits systemic risk also reduces the implicit subsidy (and resulting competitive advantages) that accrue to the largest institutions from being seen as too big to fail. As we recently wrote regarding the Minneapolis Plan to End Too Big to Fail, such a credible regime requires realistic assumptions about the incentives for policymakers to renege on promises (including the possibility of changing existing laws) not to bail out intermediaries perceived to be systemic. It also means accepting that regulators cannot reliably anticipate crises, so that preventing them requires first and foremost that the financial system is sufficiently resilient. In our view, this means dramatically boosting capital of the largest intermediaries and using the supporting apparatus from Dodd-Frank—including (but not limited to) stress tests, living wills, the designation of systemic intermediaries, and orderly liquidation authority—to verify compliance and to permit orderly resolutions in cases where failure threatens the financial system as a whole. Doing so should help, not hurt, small banks.

*These figures were kindly provided by Rebel A. Cole and Lawrence J. White. We also thank them for sharing their draft paper (“When Time is Not on Our Side: The Costs of Regulatory Forbearance in the Closure of Insolvent Banks”).